I’m sure that, like me, you’ve seen significant numbers of social media postings purporting to announce the death, or at the very least, the decline of compliance work.

Personally, I just don’t buy it.

Published views appear to be polarising; some adamant that compliance as we know it is here to stay, others that advisory is the way forward. Compliance work is a huge part of what accountants do for clients and MTD will make it even more important, so announcements of the death of compliance seem somewhat premature. However, the world of compliance is undoubtedly changing, and has been doing so for some time. Cloud accounting software has radically changed the way that accountants operate and the increased adoption of software driven by MTD is undoubtedly building on this. Whilst increased adoption potentially puts downward pressure on fees though increased competition, it also offers big opportunities to achieve significant operational efficiencies. How accountants respond to this change depends entirely on their own aspirations and goals.

I’m not a great fan of trying to “pigeonhole” accounting firms into neat little boxes; after all, within in any given market, there are usually several different business models that operate successfully alongside each other, often overlapping. What’s important is to understand what each accounting firm wants to achieve and what it wants to provide its clients.

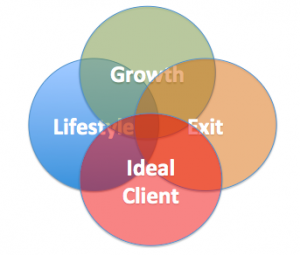

I talk to accounting firms every day, and broadly speaking I see variations on four key business models:

Lifestyle – the primary objective is to generate sufficient income to support specific lifestyle goals, whether that’s earnings, working hours, building a pension, or multiple holidays each year.

Growth – driven by growth in terms of the number of clients supported, or the range of services offered, or both.

Exit planning – driven by a specific exit goal at some point in the future, whether that’s exit by sale, or perhaps passing the firm to a family member, partner or management team.

Ideal Client – these firms have identified the characteristics of the ideal client that they want to work with, whether that’s a specific vertical market, business size, location, employee numbers etc.

It’s important to point out that these models are by no means mutually exclusive; An individual firm can successfully operate aspects of multiple models – which is why I think it’s dangerous and arguably pointless trying to pigeonhole firms.

In each of these four approaches, compliance and advisory services sit side by side; it’s just the proportion of time spent on and revenues generated from each that varies. After all, even those firms who only offer compliance services still provide advice to their clients, (although they may not actually charge for it).

So is compliance dead or dying and should a firm be changing its business model?

For me, that’s the wrong question for firms to be asking. A much more valuable question to ask is “What are the business and personal goals that the firm’s owners aspire to”? Once these are defined, then a suitable business model can be selected that supports achieving those goals.

The next step is to develop a well thought out business plan that clearly sets out the financial and operational goals, the timeframes and specific actions required to achieve them. With this in place, firms can focus on attracting and supporting the right type of client who needs and wants the type of services that the firm wants to offer.

For those firms that do wish to provide extensive guidance to their clients to help them run their businesses more successfully, then there are a wide range of tools available like The Gap to help support this activity, or specialists like Proten Sales Development to help in areas where the accountant doesn’t have specific expertise. And, of course, who better to advise a client on how to structure and run their business effectively, than an accountant who has gone through the exact same exercise on their own business.

If you found this article useful, don’t forget to subscribe to receive regular tips and ideas via the form below!